Loan app without BVN searches represent one of the biggest misconceptions among Nigerian borrowers today. After helping several family members in London apply for loans, I have realised that a proper understanding of BVN and related requirements can save you time and disappointment.

My younger brother searched for weeks for a non BVN loan before I explained what will happen in 2025. Now all recognized lenders ask for Bank Verification Number for validity and safety of customers.

The Central Bank of Nigeria legalised the use of BVN for all financial services to safeguard lenders and borrowers. This article will explain why and what alternatives are available for different situations.

Understanding BVN Requirements for Loan Apps

The quest for a loan app without BVN is authentic, but things have fundamentally changed since 2023.

Why CBN Made BVN Compulsory

Regulatory compliance reasons:

- Anti money laundering (AML) requirements under federal law

- Standards for financial institutions to Know Your Customer

- Consumer protection through verified identity systems

- Credit bureau reporting for national financial inclusion

- Fraud prevention and identity theft protection

- International banking standard compliance requirements

- Financial crimes prevention and investigation support

- National financial data integration and security

- Cross border transaction monitoring capabilities

- Terrorist financing prevention and detection systems

Consumer protection benefits:

- Prevents identity theft and impersonation

- Ensures only verified individuals access credit

- Protects borrowers from fraudulent loan applications

- Creates accountability for both lenders and borrowers

- Enables proper dispute resolution mechanisms

- Provides legal recourse for financial crimes

- Supports credit history building and tracking

- Facilitates financial inclusion through verified identity

- Enables government financial support program access

- Creates foundation for national digital identity system

What BVN Provides to Lenders

Risk assessment capabilities:

- Verified identity confirmation across banking system

- Transaction history analysis for creditworthiness

- Employment verification through salary account tracking

- Debt obligation visibility across multiple institutions

- Geographic location verification for service delivery

- Age and identity document verification

- Bank account activity monitoring and analysis

- Credit facility usage patterns across institutions

- Financial behavior analysis for loan decisions

- Fraud detection through cross institutional data sharing

Operational efficiency benefits:

- Automated customer verification processes

- Reduced manual document verification requirements

- Faster loan processing through verified data access

- Lower operational costs for customer onboarding

- Improved customer service through verified information

- Enhanced collection processes through verified contacts

- Streamlined compliance reporting to regulators

- Reduced fraud losses and operational risks

- Improved loan portfolio quality through better screening

- Enhanced customer relationship management capabilities

How to Get Your BVN for Loan Applications

Since no loan app without BVN is available anymore, obtaining your BVN becomes essential for accessing money making apps and financial services.

BVN Registration Process

Bank branch registration:

- Visit any Nigerian bank branch with valid identification

- Complete BVN enrollment form with accurate information

- Provide biometric data (fingerprints and photograph)

- Submit valid government issued identification document

- Provide current contact information and address

- Complete know your customer documentation requirements

- Pay applicable registration fees if required

- Receive temporary BVN receipt for immediate use

- Wait 24 to 48 hours for BVN activation across banking system

- Verify BVN status through USSD code after activation

Required documents for BVN registration:

- National Identity Card (NIN) or driver’s license

- International passport (if available)

- Voter registration card (as supporting document)

- Birth certificate (for age verification)

- Certificate of origin or local government identification

- Utility bill for address verification (recent)

- Employment letter or business registration documents

- Passport photographs (recent colored copies)

- Marriage certificate (if name changed through marriage)

- Court affidavit for name changes (if applicable)

BVN Retrieval Methods

USSD code retrieval:

- Dial 5650# from phone number linked to bank account

- Authenticate your identity via security questions

- Receive BVN via SMS on registered phone number

- Note BVN immediately for future loan applications

- Verify BVN works across different bank platforms

- Update phone number if not receiving SMS

- Contact bank directly if USSD method fails

- Keep BVN confidential and secure from unauthorized access

- Use BVN only for legitimate financial transactions

- Report BVN compromise immediately to banks and authorities

Bank inquiry methods:

- Visit bank branch with valid identification

- Call customer service hotline for BVN inquiry

- Use internet banking platform BVN lookup feature

- Check mobile banking app for BVN display

- Request BVN through bank’s official website

- Use bank’s WhatsApp service for BVN retrieval

- Visit ATM for BVN inquiry (where available)

- Email bank customer service with verification documents

- Use bank’s social media channels for assistance

- Contact bank relationship manager for personal assistance

Alternative Verification for Special Cases

While no loan app without BVN exists, alternative verification methods help specific user groups access credit alongside business opportunities.

Students and Young Adults

Student loan alternatives without traditional employment:

- Family guarantee systems through microfinance institutions

- Educational institution partnership loan programs

- Scholarship advance programs from educational foundations

- Peer to peer lending platforms with student categories

- Community development financial institution programs

- Religious organization educational support programs

- State government student loan scheme applications

- Federal government educational loan programs

- Professional association educational support funds

- Alumni association support programs for current students

Documentation for student verification:

- Valid student identification card and enrollment letter

- School fee payment receipts and academic transcripts

- Parental or guardian income verification documents

- National Youth Service Corps (NYSC) documents if applicable

- Part time employment verification from employers

- Scholarship award letters and educational grants

- Bank account statements showing financial support

- Academic performance records and recommendation letters

- Future employment prospects and career planning documents

- Social media presence and digital footprint verification

Rural and Unbanked Populations

Microfinance institution alternatives:

- Community based microfinance cooperatives

- Village savings and loan associations (VSLAs)

- Agricultural cooperative society lending programs

- Women’s group collective lending initiatives

- Artisan and trader association loan programs

- Religious organization financial support systems

- Traditional rotating savings groups (contributory schemes)

- Local government poverty alleviation loan programs

- Non governmental organization microcredit programs

- International development organization funding programs

Documentation for rural verification:

- Local government area identification certificates

- Traditional ruler attestation letters

- Community leader recommendation letters

- Land ownership documents and property verification

- Agricultural production records and income documentation

- Trade association membership certificates

- Religious organization membership verification

- Cooperative society membership documentation

- Local business registration and operation permits

- Community social verification through group guarantees

Informal Sector Workers

Alternative credit assessment methods:

- Mobile money transaction history analysis

- Business location verification and customer testimonials

- Trade association membership and recommendation systems

- Supplier and customer reference verification

- Social network analysis and community standing

- Business asset verification and ownership documentation

- Market association membership and fee payment records

- Utility bill payment history and residence verification

- Professional guild membership and skills certification

- Community development project participation records

Documentation alternatives:

- Business registration with local government authorities

- Tax identification number and payment receipts

- Professional association membership certificates

- Trade permit and business operation licenses

- Market association dues payment receipts

- Supplier invoice and payment history records

- Customer testimonial letters and references

- Business asset inventory and ownership proof

- Professional skills certification and training records

- Community leadership roles and social contributions

Digital Identity Alternatives

The future of verification beyond traditional loan app without BVN searches includes emerging digital identity solutions for those exploring affiliate marketing.

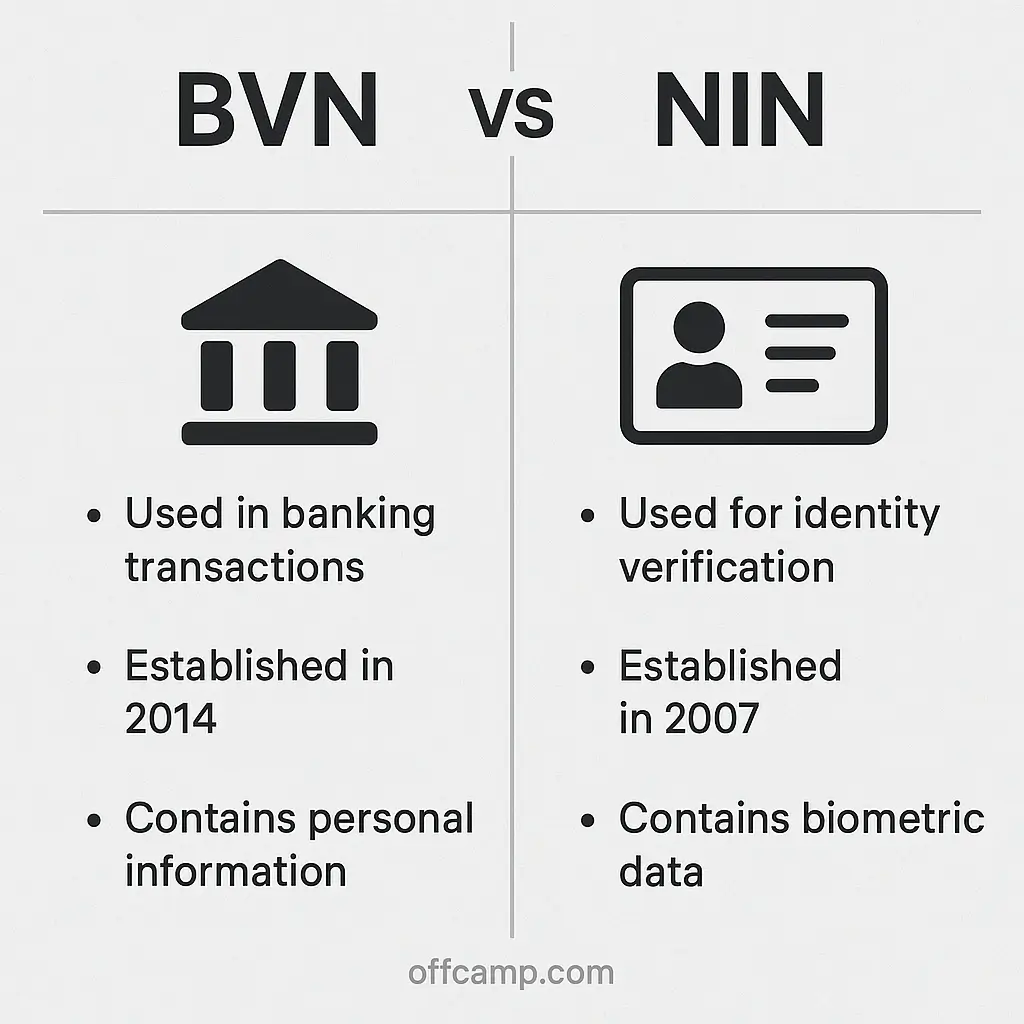

National Identity Number (NIN) Integration

NIN as primary verification:

- National Identity Management Commission enrollment

- Biometric data linking across government systems

- Social services integration through verified identity

- Healthcare system access through NIN verification

- Educational system enrollment and tracking

- Employment verification and professional registration

- Voter registration and civic participation tracking

- Tax system integration and compliance monitoring

- Border control and international travel documentation

- Digital service access and online verification systems

NIN enrollment process:

- Visit NIMC enrollment center with required documents

- Capture biometric data completely (fingerprints, photo, signature)

- Provide demographic information and supporting documents

- Pay enrollment fees and processing charges

- Receive temporary enrollment slip with tracking number

- Wait for NIN generation and card production

- Collect NIN card from designated pickup center

- Link NIN to existing bank accounts and financial services

- Update NIN information with life changes and relocations

- Use NIN for various official and commercial transactions

Mobile Money Integration

Alternative financial service access:

- Mobile network operator financial services

- Agent banking through telecommunications partnerships

- Prepaid card systems linked to mobile accounts

- Digital wallet services with alternative verification

- Peer to peer transfer systems with social verification

- Merchant payment systems with transaction history

- Utility payment history as credit verification basis

- Airtime purchase patterns for financial behavior analysis

- Data subscription patterns for income assessment

- Mobile money agent relationship and transaction verification

Mobile based verification methods:

- Phone number ownership verification through network operators

- Social network analysis through contact lists and communication

- Location verification through cellular tower data

- Device fingerprinting for unique user identification

- App usage patterns for behavioral analysis

- Mobile payment history for financial assessment

- Social media presence and digital reputation

- Online marketplace participation and ratings

- Digital skills demonstration through technology usage

- Community engagement through mobile platforms

Cryptocurrency and Blockchain Solutions

Decentralized finance (DeFi) alternatives:

- Peer to peer lending platforms using cryptocurrency

- Blockchain based identity verification systems

- Smart contract loan agreements with alternative collateral

- Cryptocurrency savings and lending protocols

- Decentralized autonomous organization (DAO) lending

- Cross border remittance backed lending systems

- Tokenized asset backed lending platforms

- Blockchain credit scoring through transaction history

- Decentralized insurance and risk management systems

- Community governed lending pools and mutual aid

Cryptocurrency backed loan requirements:

- Digital wallet ownership and transaction history

- Cryptocurrency holdings as collateral verification

- Blockchain transaction patterns for credit assessment

- Decentralized identity verification through blockchain

- Smart contract interaction history and reputation

- Cryptocurrency mining or staking participation

- Digital asset portfolio diversity and management

- Blockchain based social and professional networks

- Decentralized application usage and engagement

- Community participation in blockchain governance

Preparing for Future Loan Applications

BVN optimization strategies:

- Maintain active bank account with regular transactions

- Build positive banking relationship through consistent savings

- Keep contact information updated across all bank accounts

- Monitor credit score improvement through verified financial behavior

- Diversify banking relationships with multiple institutions

- Maintain employment records and income documentation

- Build references through professional and social networks

- Participate in formal financial system through documented transactions

- Avoid financial impropriety that could affect BVN status

- Stay informed about regulatory changes and compliance requirements

Building creditworthiness:

- Start with small loan amounts and perfect repayment records

- Use multiple financial services to build comprehensive history

- Maintain stable employment and document income growth

- Build emergency fund to ensure loan repayment capability

- Avoid excessive debt and maintain healthy credit utilization

- Pay all bills on time to demonstrate financial responsibility

- Build professional network and character references

- Engage with financial education and literacy programs

- Monitor credit reports and correct errors promptly

- Plan major financial decisions and communicate with lenders

Regulatory Future and Industry Trends

Expected regulatory developments:

- Enhanced consumer protection regulations for digital lending

- Standardized interest rate caps and fee limitations

- Improved dispute resolution mechanisms and consumer advocacy

- Integration with national social protection programs

- Enhanced financial inclusion initiatives for underserved populations

- Strengthened data protection and privacy requirements

- International regulatory cooperation and best practice adoption

- Technology innovation sandbox for new financial products

- Enhanced credit reporting and bureau system improvements

- Simplified BVN processes while maintaining security standards

Industry innovation trends:

- Artificial intelligence for enhanced credit scoring

- Blockchain technology for secure identity verification

- Open banking initiatives for improved financial data access

- Biometric authentication beyond traditional BVN requirements

- Internet of Things (IoT) integration for alternative verification

- Machine learning for fraud detection and prevention

- Digital asset integration for alternative collateral systems

- Cross border lending and remittance integration

- Financial wellness and education platform integration

- Sustainable finance and environmental impact lending

Scam Prevention: Fake Loan App Without BVN

Common scam tactics to avoid:

- Apps claiming to offer loans without BVN requirements

- Upfront fee requests before loan approval or disbursal

- Unrealistic loan amounts for unverified applicants

- Pressure tactics demanding immediate personal information

- Unofficial app stores and unverified download sources

- Social media advertisements for guaranteed approvals

- Email or SMS offers bypassing official app channels

- Requests for banking passwords or PIN information

- Promises of loans without credit checks or verification

- Third party intermediaries claiming special access

Red flags indicating fraudulent operations:

- No physical address or legitimate customer service

- Absence from official regulatory approval lists

- Extremely low interest rates that seem too good to be true

- Immediate approval promises without any verification

- Poor grammar and spelling in official communications

- No clear terms and conditions or loan agreements

- Requests for payments to process or guarantee loans

- No customer reviews on legitimate platforms

- Pressure to make quick decisions without research time

- Lack of clear complaints or dispute resolution procedures

Protection strategies:

- Verify all lenders through CBN and FCCPC official lists

- Research company background and customer reviews thoroughly

- Never pay upfront fees for loan processing or approval

- Protect BVN and banking information from unauthorized access

- Report suspected fraudulent operations to authorities

- Use only official app stores for legitimate app downloads

- Verify customer service contacts through official channels

- Read and understand all terms before accepting loan offers

- Seek advice from trusted financial advisors when uncertain

- Document all interactions with potential lenders for protection

Building Emergency Fund Instead of Seeking Loan App Without BVN

Emergency fund building strategies:

- Start with small amounts that fit your current budget

- Automate savings transfers to reduce temptation to spend

- Use separate high yield savings accounts for emergency funds

- Set realistic goals starting with ₦10,000 first milestone

- Celebrate progress milestones to maintain motivation

- Find additional income sources to accelerate fund growth

- Reduce unnecessary expenses and redirect to emergency savings

- Use windfalls like bonuses or gifts for emergency fund building

- Track progress visually through charts or apps

- Review and adjust savings goals based on changing circumstances

Emergency fund targets by income level:

- Monthly income ₦30,000 to ₦50,000: Target ₦50,000 to ₦100,000 fund

- Monthly income ₦50,000 to ₦100,000: Target ₦150,000 to ₦300,000 fund

- Monthly income ₦100,000 to ₦200,000: Target ₦300,000 to ₦600,000 fund

- Monthly income ₦200,000+: Target 6 months of expenses minimum

- Student/irregular income: Target ₦25,000 to ₦50,000 starter fund

- Business owners: Target higher amounts due to income volatility

- Single parents: Prioritize emergency fund over other savings

- Retirees: Maintain larger emergency funds for health expenses

- Young professionals: Build emergency fund before other investments

- Rural residents: Account for limited financial service access

Consider exploring profitable business ventures or investment platforms to build multiple income streams.

Financial Education Resources

Developing financial literacy:

- Central Bank of Nigeria financial education programs

- University and polytechnic personal finance courses

- Online financial education platforms and mobile apps

- Professional financial advisor consultation services

- Community based financial literacy training programs

- Religious organization financial stewardship programs

- Employer sponsored financial wellness workshops

- Professional association financial planning seminars

- Government financial inclusion and education initiatives

- International development organization training programs

Key financial skills to develop:

- Budgeting and expense tracking for better money management

- Understanding interest rates and loan calculations

- Credit score management and improvement strategies

- Emergency fund planning and implementation

- Investment basics and long term wealth building

- Insurance planning for risk management

- Tax planning and compliance understanding

- Business financial management for entrepreneurs

- Retirement planning and pension optimization

- Estate planning and wealth transfer strategies

Community Based Alternatives

Traditional financial support systems:

- Family and extended family support networks

- Community rotating savings and credit associations

- Religious organization mutual aid societies

- Professional guild and association support funds

- Ethnic association and hometown union assistance

- Women’s group collective savings and lending

- Youth association peer support networks

- Market trader association cooperative lending

- Farmer cooperative seasonal credit programs

- Artisan guild emergency assistance funds

Modern community finance innovations:

- Online peer to peer lending platforms

- Social media based community funding groups

- Crowdfunding platforms for personal emergencies

- Digital savings groups and investment clubs

- Professional network mentorship and support

- Alumni association support networks

- Entrepreneur and startup community funding

- Skill sharing and service exchange networks

- Community development finance institutions

- Social impact investing and community focused funds

You can also explore online business opportunities and legitimate games that pay as alternative income sources.

Legal Rights and Consumer Protection

Consumer rights in digital lending:

- Right to transparent terms and conditions

- Protection from harassment and abusive collection practices

- Right to dispute resolution and complaint procedures

- Privacy protection for personal and financial information

- Right to fair and non discriminatory lending practices

- Protection from predatory lending and excessive interest rates

- Right to loan modification and restructuring in hardship

- Access to regulatory complaint mechanisms

- Right to credit reporting accuracy and dispute resolution

- Protection from fraud and identity theft

Regulatory protection agencies:

- Federal Competition and Consumer Protection Commission (FCCPC)

- Central Bank of Nigeria (CBN) consumer protection department

- Nigerian Communications Commission (NCC) for telecom related issues

- Economic and Financial Crimes Commission (EFCC) for fraud cases

- Consumer Protection Agencies in each state

- Banking Ombudsman for dispute resolution

- Credit Bureau complaint and dispute mechanisms

- Legal Aid Council for low income consumer protection

- Nigerian Bar Association consumer rights advocacy

- Civil society organizations focused on financial consumer protection

International Best Practices

Global trends in financial inclusion:

- Mobile money expansion in developing countries

- Alternative credit scoring using non traditional data

- Regulatory sandboxes for financial technology innovation

- Open banking initiatives for improved financial access

- Digital identity systems for financial service access

- Financial education integration with digital services

- Consumer protection enhancement in digital lending

- Cross border remittance and lending integration

- Sustainable finance and environmental impact consideration

- Financial wellness and behavioral finance application

Lessons from other African countries:

- Kenya’s M Pesa mobile money success model

- Ghana’s digital financial services regulation framework

- South Africa’s credit bureau and scoring system

- Rwanda’s cashless economy and digital payment integration

- Tanzania’s mobile banking and rural financial inclusion

- Uganda’s agricultural finance and seasonal lending models

- Ethiopia’s diaspora remittance and investment programs

- Morocco’s Islamic finance and alternative banking

- Egypt’s fintech regulatory framework development

- Botswana’s financial consumer protection mechanisms

Consider exploring affiliate marketing platforms or virtual assistant opportunities to supplement your income.

Building Long Term Financial Stability

Instead of searching for a loan app without BVN, focus on building sustainable financial health.

Income Diversification Strategies

Multiple income streams:

- Explore legitimate online earning opportunities

- Develop skills for freelance work and consulting

- Consider small business ventures within your expertise

- Investigate passive income through investments

- Build expertise in high demand digital skills

- Participate in the gig economy through verified platforms

- Monetize hobbies and personal interests

- Create educational content and online courses

- Offer professional services in your field

- Develop intellectual property and licensing opportunities

Financial Planning Framework

Systematic wealth building:

- Create detailed monthly budgets and stick to them

- Establish multiple savings goals for different purposes

- Invest in continuous education and skill development

- Build professional networks for career advancement

- Plan for major life events and associated costs

- Diversify investments across different asset classes

- Maintain adequate insurance coverage for major risks

- Develop multiple retirement savings strategies

- Create estate planning documents for wealth transfer

- Regularly review and adjust financial plans

Frequently Asked Questions About BVN and Loan App Requirements

Correct, all legitimate loan apps now require BVN per CBN regulations for consumer protection and anti fraud measures.

Visit any Nigerian bank branch with valid ID to register for BVN, or dial 5650# if you have existing bank account.

Yes, BVN registration doesn’t require employment, just valid identification and basic account opening requirements.

Bank branch registration takes 30 to 60 minutes, with BVN activation across banking system within 24 to 48 hours.

Legitimate apps must comply with data protection regulations, but only use licensed lenders for security.

Microfinance institutions, cooperative societies, and community based lending may have different requirements.

No, using another person’s BVN is illegal and constitutes identity fraud with serious legal consequences.

Licensed lenders follow data protection laws, but read privacy policies carefully before sharing information.

Contact your bank immediately to update information and recover BVN access through proper verification procedures.

International lenders may have different requirements, but most still require significant verification and documentation.

Future of Digital Identity and Lending

The evolution beyond loan app without BVN concepts includes exciting technological developments.

Emerging Technologies

Next generation verification:

- Artificial intelligence powered identity verification

- Blockchain based decentralized identity systems

- Biometric authentication using facial recognition

- Voice pattern recognition for identity confirmation

- Behavioral biometrics for continuous authentication

- Internet of Things integration for lifestyle verification

- Social graph analysis for identity confirmation

- Machine learning algorithms for fraud detection

- Quantum cryptography for enhanced security

- Augmented reality interfaces for identity verification

Policy Development

Regulatory innovation:

- Sandbox environments for testing new technologies

- Consumer protection frameworks for digital innovation

- Cross border cooperation for international transactions

- Privacy preserving identity verification protocols

- Financial inclusion metrics and accountability systems

- Digital rights frameworks for financial services

- Interoperability standards for identity systems

- Environmental sustainability requirements for fintech

- Accessibility standards for disabled users

- Cultural sensitivity guidelines for diverse populations

{kind=link}